At this time last year, economists were predicting that inflation would swiftly fade in 2022 as supply chain issues cleared, consumers shifted from goods to services spending and pandemic relief waned. They are now forecasting the same thing for 2023, citing many of the same reasons.

But as consumers know, predictions of a big inflation moderation this year were wrong. While price increases have started to slow slightly, they are still hovering near four-decade highs. Economists expect fresh data scheduled for release on Tuesday to show that the Consumer Price Index climbed by 7.3 percent in the year through November.

That begs the question: Should America believe this round of inflation optimism?

“There is better reason to believe that inflation will fall this year than last year,” said Jason Furman, an economist from Harvard who was skeptical of last year’s forecasts for a quick return to normal. Still, “if you pocket all the good news and ignore the countervailing bad news, that’s a mistake.”

Economists are slightly less optimistic than last year.

Economists see inflation fading notably in the months ahead, but after a year of foiled expectations, they aren’t penciling in quite as drastic a decline as they were last December.

The Fed officially targets the Personal Consumption Expenditures index, which is related to the consumer price measure. Officials particularly watch a version of the number that illustrates underlying inflation trends by stripping out volatile food and fuel prices — so those forecasts give the best snapshot of what experts are anticipating.

Last year, economists surveyed by Bloomberg expected that so-called core index to fall to 2.5 percent by the end of 2022. Instead, it is running at 5 percent, twice that pace.

This year, forecasters expect inflation to fade to 3.5 percent by the end of 2023.

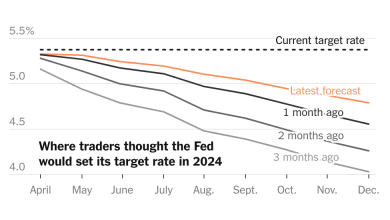

The Federal Reserve’s predictions have followed a similar pattern. As of last December, central bankers expected core inflation to end 2022 at 2.7 percent. Their September projections showed price increases easing to 3.1 percent by the end of next year. Fed officials will release a new set of inflation forecasts for 2023 on Wednesday following their December policy meeting.

Supply chains are healing.

One reason to think that the anticipated but elusive inflation slowdown will finally show up in 2023 ties back to supply chains.

At this time last year, economists were hopeful that snarls in global shipping and manufacturing would soon clear; consumer spending would shift away from goods and back to services; and the combination would allow supply and demand to come back into balance, slowing price increases on everything from cars to couches. That has happened, but only gradually. It has also taken longer to translate into lower consumer prices than some economists had expected.

Inflation F.A.Q.

What is inflation? Inflation is a loss of purchasing power over time, meaning your dollar will not go as far tomorrow as it did today. It is typically expressed as the annual change in prices for everyday goods and services such as food, furniture, apparel, transportation and toys.

What causes inflation? It can be the result of rising consumer demand. But inflation can also rise and fall based on developments that have little to do with economic conditions, such as limited oil production and supply chain problems.

Is inflation bad? It depends on the circumstances. Fast price increases spell trouble, but moderate price gains can lead to higher wages and job growth.

How does inflation affect the poor? Inflation can be especially hard to shoulder for poor households because they spend a bigger chunk of their budgets on necessities like food, housing and gas.

Can inflation affect the stock market? Rapid inflation typically spells trouble for stocks. Financial assets in general have historically fared badly during inflation booms, while tangible assets like houses have held their value better.

But the expected shift is finally, if belatedly, showing up. After months of supply chain healing, consumers are now beginning to feel the benefit. Used car prices began declining meaningfully in October inflation data, furniture prices are slumping and apparel is falling in price. Similar cost declines are expected to weigh on inflation next year.

“It is far too early to declare goods inflation vanquished, but if current trends continue, goods prices should begin to exert downward pressure on overall inflation in coming months,” Jerome H. Powell, the Fed chair, said during a recent speech.

The Fed is working on cooling demand.

Unfortunately, moderation in goods prices alone would probably fail to return America to a normal inflation rate, because price increases for services have been accelerating. That category — which covers everything from meals out to monthly rent — accounted for half of consumer price inflation in October, based on a Bloomberg breakdown, up from less than a third a year earlier.

Many types of service inflation are closely intertwined with what’s happening in the job market. For companies including hair salons, restaurant chains and tax accountants, paying employees is typically a major, if not the biggest, cost of doing business. When workers are scarce and wages are climbing rapidly, businesses are more likely to raise their prices to try to cover heftier labor bills.

That means that today’s very low unemployment and abnormally rapid wage growth could help to keep price increases faster than usual, even though the job market wasn’t a big driver of the initial burst in inflation.

That is where Fed policy could come in. Companies can only charge more if their customers are able — and willing — to pay more. The Fed can stop that chain reaction by lifting interest rates to slow demand.

Policymakers have raised interest rates from near-zero at the start of 2022 to nearly 4 percent, and are expected to make another interest rate increase this week. Those moves have made it more expensive to borrow money to buy a house, finance a big purchase or expand a business.

The knock-on effects are now trickling through the economy: Fewer house sales could eventually mean less hiring in construction and manufacturing, which in turn would mean less spending in the local economies where would-be builders and factory workers live. As the job market slows down and wage growth moderates, demand is expected to weaken for everything from dinners out to air travel.

Understand Inflation and How It Affects You

- Social Security: The cost-of-living adjustment, which helps the benefit keep pace with inflation, will be 8.7 percent next year. Here is what that means.

- Budget Surpluses: Up to 20 states are using their excess funds to help taxpayers deal with rising costs. But some economists worry that the payments could fuel inflation.

- Tax Rates: The I.R.S. has made inflation adjustments for 2023, which could push many people into a lower tax bracket and reduce tax bills.

- Your Paycheck: Inflation is taking a bigger and bigger bite out of your wallet. Now, it’s going to affect the size of your paycheck next year.

“Slower wage growth will reduce upward pressure on services inflation,” economists at Goldman Sachs predicted. But the process might take time. They expect the labor market for health care workers in particular to remain hot and put upward pressure on inflation next year, for instance.

Rent growth is moderating.

In one service category, though, a 2023 inflation deceleration is a fairly sure bet: rents.

Rent increases take time to flow into measured inflation because existing tenants do not start paying more until they renew their leases. That means that a 2021 pop in new rents has been slowly working its way into the official price numbers, pushing up inflation throughout 2022.

Market-based rents have begun to cool or even fall in recent months, which suggests that rent growth should also begin to moderate. The uncertainty is when the slowdown will happen — some economists think as early as next spring — and how quickly rents will decelerate.

But big wild cards remain.

The challenge with forecasting inflation is that while it is possible to make guesses about specific categories like rent, many inflation drivers come as a surprise. Forecasters in 2021 could not have guessed that Russia would invade Ukraine in early 2022, sharply pushing up food and fuel prices.

Likewise, it is hard to guess what will happen on the geopolitical stage next year. An escalation of the conflict in Europe could put renewed pressure on gas prices. The return of Chinese consumers after years of rolling lockdowns could lead to more people competing for goods in the global market.

And things could simply take longer than expected to return to normal. That’s partly what happened in 2022. Consumption and the labor market both outstripped expectations, keeping the pressure on prices.

“The economy was more resilient than expected,” said Laura Rosner-Warburton, senior economist at Macro Policy Perspectives. “Supply chain problems lasted a lot longer than expected and have been difficult to forecast on the way up and down.”

How quickly demand will slow is still uncertain. The labor market is expected to cool, but for now it is strong. And many households are still in solid financial shape. They amassed $2.3 trillion in extra savings during the pandemic thanks to months stuck at home and government stimulus, and still had about $1.7 trillion of that by mid-2022, based on Fed research.

Those nest eggs have helped Americans to sustain their spending this year, giving companies the ability to raise prices without scaring away customers — a trend that could continue, at least for a while.

The challenge in forecasting, Mr. Furman said, is that there’s “a powerful desire to tell a happy story.” So far, inflation has been anything but.